Go paper-free

Amend paper-free preferences for your statements and correspondence.

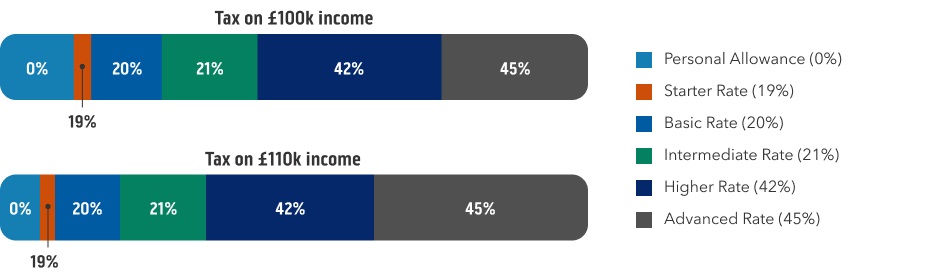

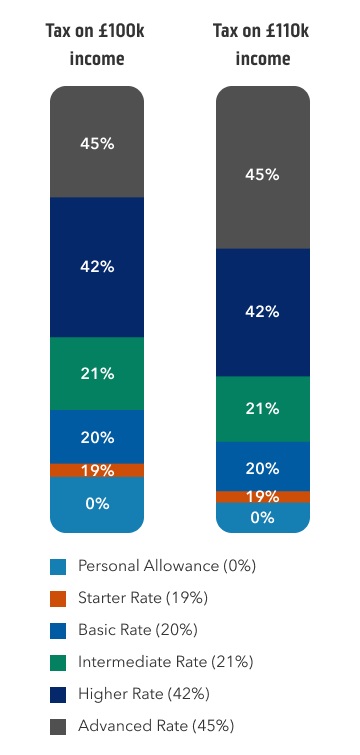

If you earn between £100,000 and £125,140, make sure you avoid the tax trap.

You probably know that the advanced rate of tax is 45%, but did you know that you could be paying an effective rate of 67.5% tax on some of your income?

On this page, we'll cover what the tax trap is, who it catches, and a way you can avoid it. You can also watch our video (1min 36secs).

If you live in England, Northern Ireland or Wales, tax rates are different, but the same tax trap still exists.

If you earn £100,000 and receive a £1,000 bonus, your bonus pushes your earnings above the £100,000 limit. This means you'll start to lose some of your personal allowance.

This means you'll face an effective tax rate of 67.5% on the amount over £100,000. In this case, you'll only keep £375 of the extra income. The bonus will also be subject to National Insurance, leaving you with less in your pay cheque.

Remember, it's not just a bonus that can push you over the threshold. HMRC considers all sources of income when it calculates your income tax for each tax year. This includes your salary, dividends, certain types of rental income, and interest. It's important to think about the bigger picture.

Because of the way tax relief works on most personal pension schemes, if you’re paying a higher rate of tax and saving into a personal pension, it’s important to complete a Self-Assessment so you can claim the tax relief back that you’re entitled to.

You can read the government website for a full list of who legally must complete a Self-Assessment. This includes anyone earning over £150,000 or who has received any untaxed income, for example from a rental property or dividends.

If you’re expecting your income to exceed £100,000 this year, it could be worth checking with your employer to see if it’s possible to top up your workplace pension. This can make sense, especially if they offer to contribute too. Contact your employer directly to find out more.

Another option is to consider setting up a separate personal pension.

It’s easy to open a personal pension with us and start contributing straight away, either on a monthly basis or as a lump sum.

We offer two different pension options, depending on how involved you want to be in selecting investments.

By having your pension visible alongside your bank account on the app, it’s easy to keep track of.

Ready-Made Pension

Our retirement experts manage your pension investments for you, creating a portfolio that’s suitable for your age and expected retirement date.

Learn more about the Ready-Made Pension

Self-Invested Personal Pension (SIPP)

Gives you the choice of where to invest – putting you in control of your investment strategy and financial future.

Learn more about Self-Invested Personal Pensions (SIPP)

Pensions are a long-term investment. What you get back isn’t guaranteed and can go down as well as up. You could get back less than the amount(s) paid in.

The current income tax bands for Scotland are as shown in the table below.

When you reach £125,140 you lose your personal allowance completely and pay tax on every penny you earn.

It’s also the start of the additional rate tax band, meaning you’d be paying 48% tax (45% in England).

|

Band |

Taxable income |

Scottish tax rate |

|---|---|---|

|

Band Personal allowance |

Taxable income Up to £12,570 |

Scottish tax rate 0% |

|

Band Starter rate |

Taxable income £12,571 to £15,397 |

Scottish tax rate 19% |

|

Band Basic rate |

Taxable income £15,398 to £27,491 |

Scottish tax rate 20% |

|

Band Intermediate rate |

Taxable income £27,492 to £43,662 |

Scottish tax rate 21% |

|

Band Higher rate |

Taxable income £43,663 to £75,000 |

Scottish tax rate 42% |

|

Band Advanced rate |

Taxable income £75,001 to £125,140 |

Scottish tax rate 45% |

|

Band Top rate |

Taxable income Over £125,140 |

Scottish tax rate 48% |

The tax bands are different, but that doesn’t mean the tax trap doesn’t impact you. A higher rate taxpayer pays 40% in income tax, which means when you lose your personal allowance, you’re paying an effective rate of 60% tax on the income you’re earning between £100,000 and £125,140.

The current income tax bands for England, Wales and Northern Ireland are:

|

Band |

Taxable income |

Tax rate |

|---|---|---|

|

Band Personal allowance |

Taxable income Up to £12,570 |

Tax rate 0% |

|

Band Basic rate |

Taxable income £12,571 to £50,270 |

Tax rate 20% |

|

Band Higher rate |

Taxable income £50,271 to £125,140 |

Tax rate 40% |

|

Band Additional rate |

Taxable income Over £125,140 |

Tax rate 45% |

Find out more about pensions and how you could benefit from one for your retirement.

Discover how a SIPP could help you save for your retirement.